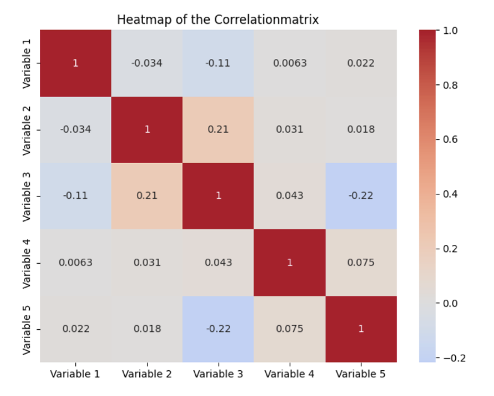

When Predictors Collide: Mastering VIF in Multicollinear Regression

In regression models, the independent variables must be not or only slightly dependent on each other, i.e. that they are not correlated. However, if such a dependency exists, this is referred to as Multicollinearity and leads to unstable models and results that are difficult to interpret. The variance inflation factor is a decisive metric for […]

When Predictors Collide: Mastering VIF in Multicollinear Regression Read More »